1 Titanium Concentrate

1.1 Weak Domestic Demand, Prices Run Weak and Stable

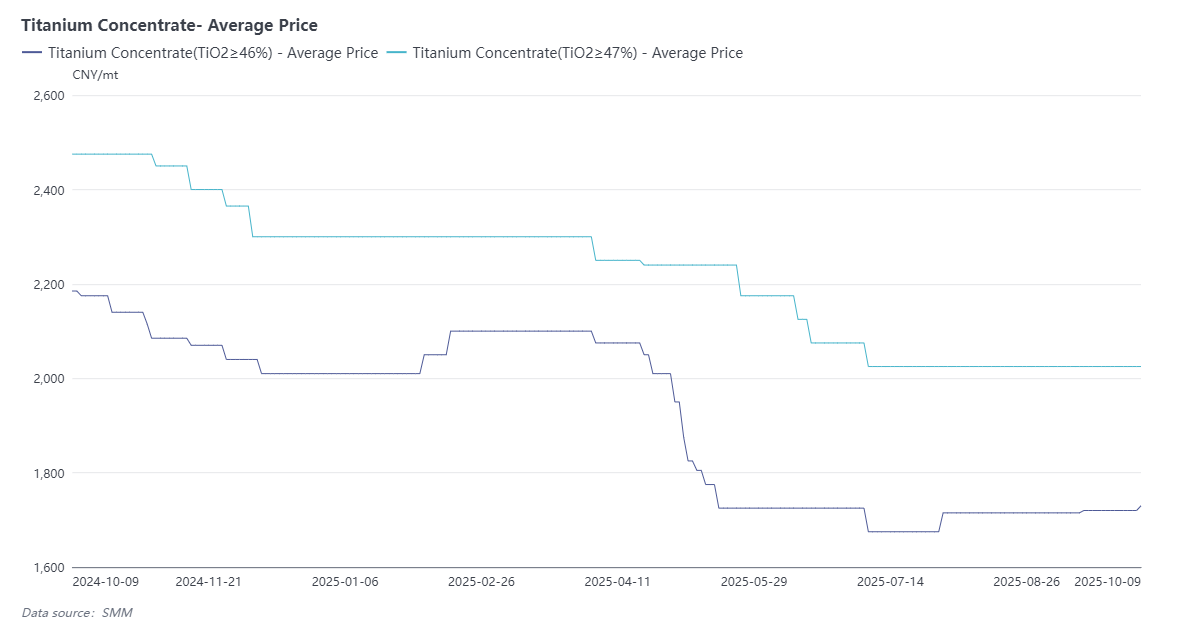

In September, the quotation range for domestic titanium concentrate (TiO₂ ≥ 46%) was 1680-1760 yuan/ton, with an average price of 1730 yuan/ton; the quotation range for TiO₂ ≥ 47% specification was 1950-2100 yuan/ton, with an average price of 2025 yuan/ton. Titanium concentrate prices overall maintained stable operation, but the trend was weak. Although influenced by the recovery in downstream titanium dioxide market demand in September, prices experienced a slight increase, the overall market did not show a significant seasonal upward trend and remained in a state of high fluctuation. The main reason is persistently weak terminal demand, which failed to effectively boost the market even during the traditional peak season "Golden September". It is expected that titanium concentrate prices will continue their weak and stable trend in October.

1.2 Import Data Insights: Sequential Recovery Masks Year-on-Year Weakness

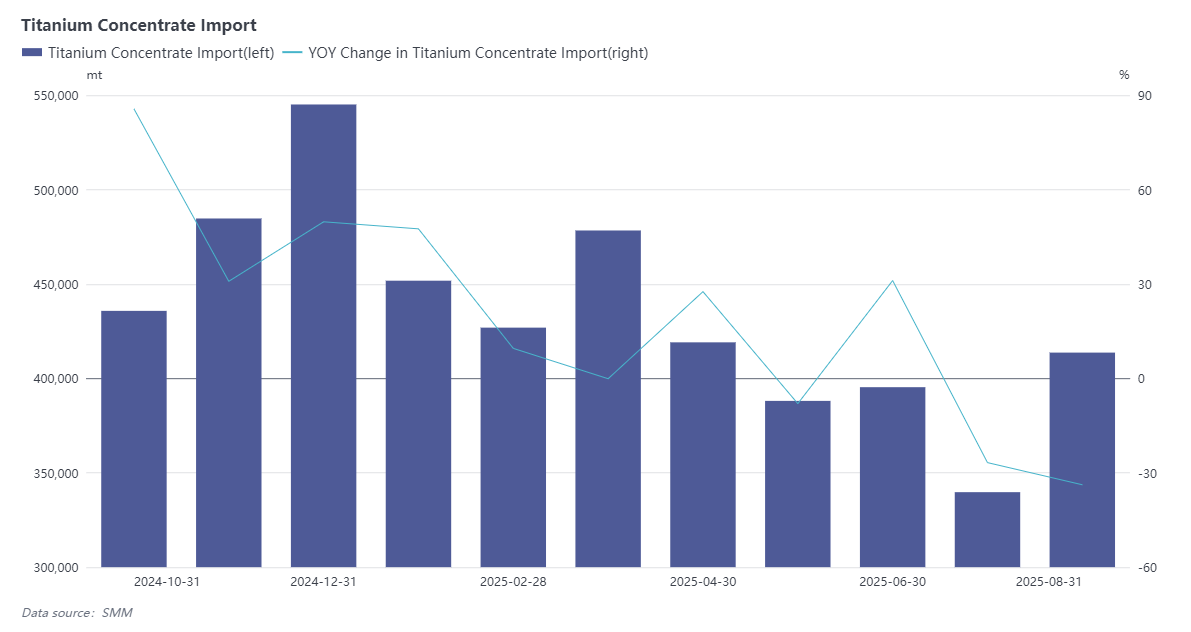

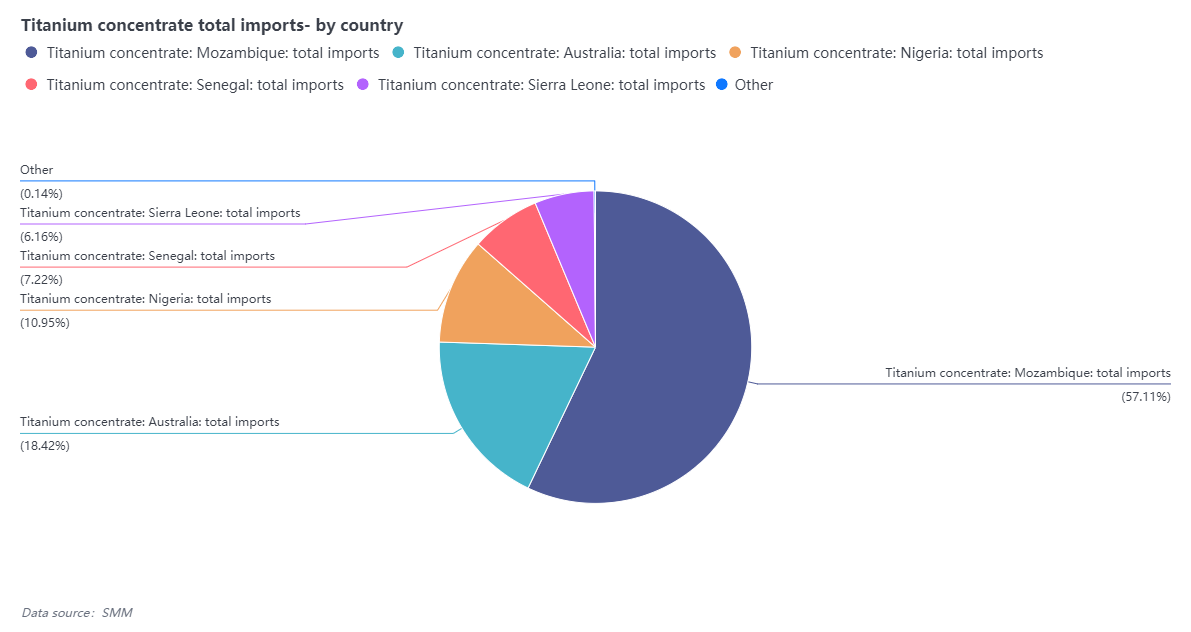

According to the latest customs data, China's titanium concentrate imports reached 413,000 tons in August 2025, a month-on-month increase of 21.76%, but still a year-on-year decrease of 33.82%; cumulative imports from January to August were 3.317 million tons, a cumulative slight decrease of 0.1% year-on-year. In terms of source countries, imports were mainly concentrated in Africa, with Mozambique being the largest supplier, importing 214,000 tons in a single month, Nigeria importing 23,000 tons, and Australia importing 41,000 tons. Although the import volume rebounded month-on-month in August, reflecting some restocking demand, the significant year-on-year decline and the weakness in cumulative data still indicate that domestic terminal demand remains generally weak, and market supply pressure has not been effectively alleviated.

2 Titanium Dioxide

2.1 Overseas Demand Drives Price Increases, Domestic Titanium Dioxide Market Experiences Narrow Fluctuations

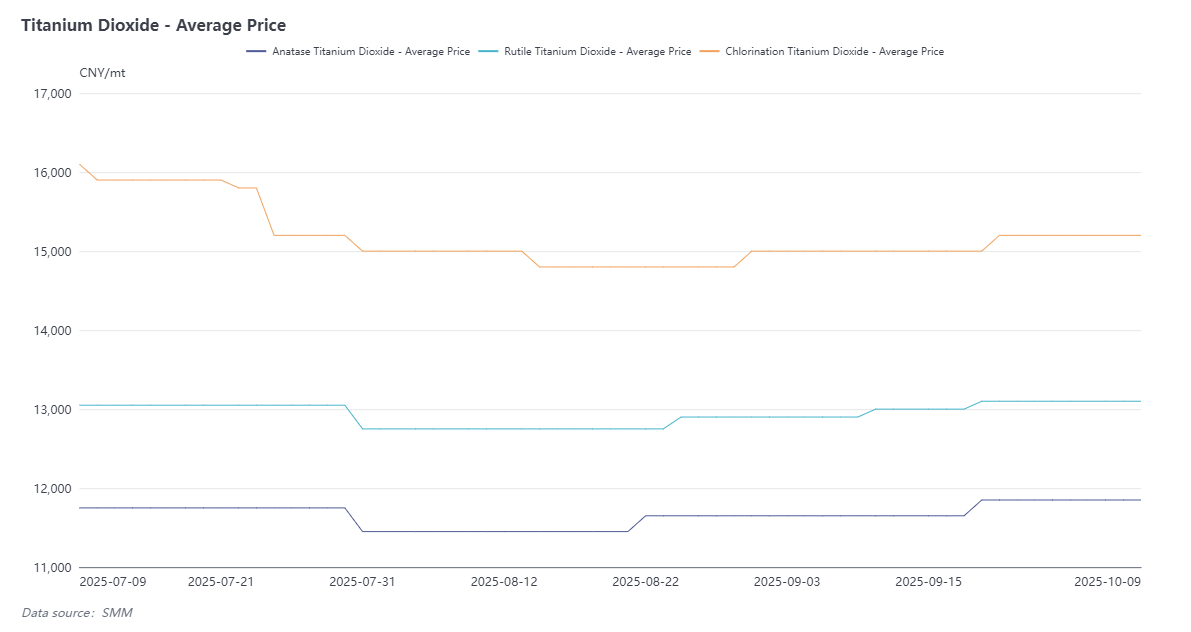

In September, the quotation for anatase titanium dioxide was 11,700-12,000 yuan/ton, with an average price of 11,850 yuan/ton; the quotation for rutile titanium dioxide was 12,800-13,400 yuan/ton, with an average price of 13,100 yuan/ton, and the average FOB price was USD 1,875/ton; the domestic quotation for chloride process titanium dioxide was 14,700-15,700 yuan/ton, with an average price of 15,200 yuan/ton, and the average FOB price was USD 2,125/ton.

Titanium dioxide prices showed an upward trend after mid-September. Since mid-September, some companies issued second price adjustment notices, pushing end-of-month quotations to maintain high levels. Following the National Day holiday, other titanium dioxide companies have also successively issued their second price adjustment notices since August to consolidate the price increase momentum. Currently, titanium dioxide quotations are at recent highs, but whether this can be sustained depends on the actual landing of new orders.

The main driving force behind this round of price increases comes from the overseas market. After Venator announced bankruptcy in September, demand for sulfate process titanium dioxide recovered, and overseas procurement willingness for Chinese products gradually increased. Additionally, on September 22, the Calcutta High Court in India ruled to cancel the anti-dumping duties on Chinese titanium dioxide, identifying major flaws in the original investigation procedure. This ruling provides short-term cost relief for Indian coating companies, but as the case is remanded to the trade remedy authority for re-examination, future policy uncertainties remain. Currently, the tariff barrier for Chinese exports to India is temporarily lifted, and whether there will be a surge in orders from the Indian market will be a key focus in October.

Overall, domestic demand has not shown significant growth. Therefore, this round of price adjustment notices in early October primarily serves to stabilize the market. Whether titanium dioxide prices can maintain the high level seen in September will largely depend on the sustainability of overseas orders. The overall price in October is expected to show a pattern of narrow fluctuations.

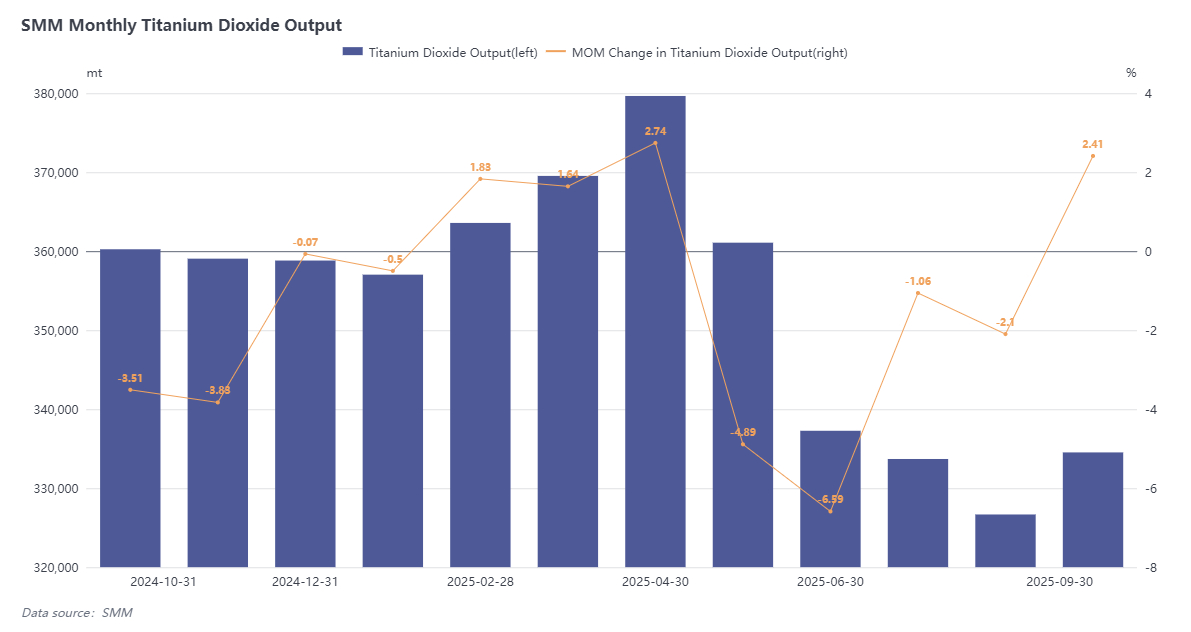

2.2 Titanium Dioxide Production Steadily Increases, Strong Demand Drives Inventory Drawdown

According to SMM data, China's titanium dioxide production was 334,500 tons in September 2025, a month-on-month increase of 2.41%. Market demand was strong this month, transaction volume increased significantly, corporate destocking effects were obvious, and overall inventory decreased by 14.03% month-on-month.

The demand growth mainly came from the sulfate process titanium dioxide market, driven by three main factors: First, the traditional "Golden September" peak season drove the recovery of domestic coating market demand; Second, influenced by the closure of Venator's German plant, European sulfate process orders shifted significantly to China, driving a surge in overseas orders; Third, the accidental shutdown of a domestic leading company's sulfate process production line intensified market expectations of tight supply.

Although some previously idled companies resumed production in September, and overall production remained stable, with the continuous depletion of inventory, many companies issued second price adjustment notices since mid-September, pushing end-of-month quotations to maintain high levels. Looking ahead to October, the sustainability of market demand remains to be seen. Against the backdrop of gradually recovering production capacity, the probability of stable production in October is high, but whether prices can continue the upward trend remains uncertain.

3 Sponge Titanium

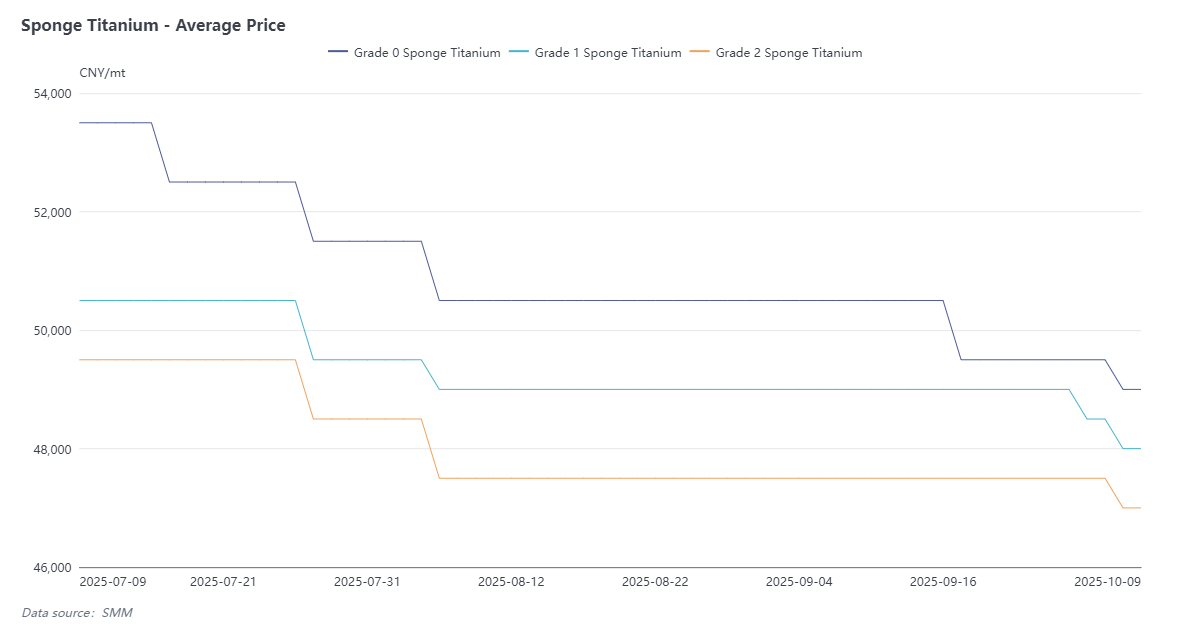

3.1 September Sponge Titanium Prices Under Pressure, High-end Demand Supports Market Divergence

The quotation for Grade 0 sponge titanium was 48,500-49,500 yuan/ton, with an average price of 49,000 yuan/ton; Grade 1 sponge titanium was quoted at 47,500-48,500 yuan/ton, with an average price of 48,000 yuan/ton; Grade 2 sponge titanium was quoted at 46,500-47,500 yuan/ton, with an average price of 47,000 yuan/ton. The overall price in September decreased by about 1,000 yuan/ton compared to the previous month, and the market showed a weak operating trend. Currently, demand for civilian-grade sponge titanium is weak, inventory has accumulated, while the high-end sponge titanium market maintains stable demand.

On September 28, the TITANIUM USA exhibition organized by the International Titanium Association (ITA) was successfully held in Boston, USA. According to the latest content released by ITA, aerospace titanium materials remain the core hotspot demand in the downstream sectors of sponge titanium. With the strong recovery of the aerospace market, the US titanium industry has made supply chain security and tariff policy its top priority. Currently, the US industry's complete reliance on imported sponge titanium poses severe challenges. Leading industry company TIMET pointed out that the current 15% import tariff puts US producers at a disadvantage in global competition, hence it actively supports the "Safeguarding American Titanium Manufacturing Act" to eliminate this tariff.

Meanwhile, consulting agency reports show that in the context of global supply chain restructuring after the Russia-Ukraine conflict, the US titanium industry is accelerating the reduction of its reliance on Russian titanium materials. Three of the four major suppliers – ATI, Howmet, and TIMET – are advancing capacity expansion plans. However, the key raw materials required for titanium alloy production involve supply chains across 36 countries, nearly 20% of which are assessed as high-risk regions. This complex situation makes establishing a diversified and stable supply chain system the most urgent strategic task for the US Titanium Association.

Looking ahead to October, sponge titanium prices are expected to continue their divergent trend: the high-end sponge titanium market is expected to continue to strengthen, driving demand for related titanium material exports; but dragged down by the civilian sector, the overall sponge titanium market will remain weak.

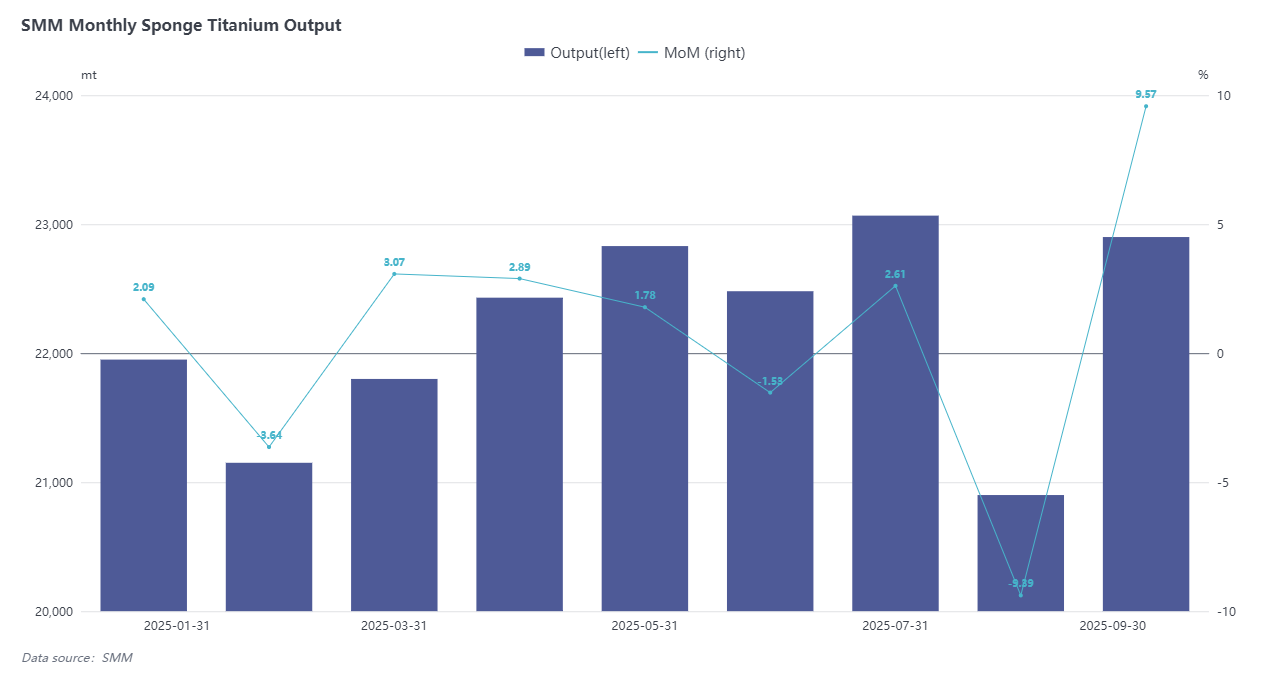

3.2 September Sponge Titanium Production Up 9.57% Month-on-Month, High-End Demand Supports Weak-Stable Pattern

According to SMM data, China's sponge titanium production was 22,900 tons in September 2025, a month-on-month increase of 9.57%. The market overall continued its weak and stable trend this month. The production recovery was mainly due to the resumption of production by some previously production-reducing enterprises in September, with no further expansion of production reduction scale in the industry.

Demand showed structural differentiation: high-end sponge titanium, supported by orders from aerospace, national defense and other high-end sectors, continued to perform strongly; while civilian sponge titanium, due to oversupply in the market, saw continuously pressured and declining prices, leading to synchronous price differentiation in the titanium materials market. From domestic and international perspectives, domestic demand recovered somewhat in September, but overall overseas demand in the third quarter was weaker than in the first half of the year, and the export market remained stable. The sponge titanium market is expected to maintain a weak supply-demand balance in October, with prices likely to continue their weak and stable trend.

4 Post-Market Forecast

In the fourth quarter of 2025, China's titanium industry chain is expected to continue the overall characteristics of "weak and stable operation, internal differentiation, and external driving". For titanium concentrate, constrained by persistently weak terminal demand, prices are expected to maintain a weak and stable pattern, lacking momentum for a trending increase. The titanium dioxide market will rely more on the support of overseas orders; the export window brought by the cancellation of Indian anti-dumping duties and the sustainability of European supply chain shifts will be key factors affecting price trends; although domestic demand is expected to recover mildly, it is unlikely to drive the market upward alone, and prices are forecast to be dominated by narrow fluctuations. The sponge titanium market will continue to show a "strong high-end, weak civilian" differentiation trend; demand in aerospace, national defense and other high-end sectors will remain robust, while the civilian sector, constrained by oversupply, will find it difficult to change the state of price pressure in the short term. Overall, the titanium industry chain lacks strong upward catalysts in the fourth quarter. Titanium enterprises should focus on overseas market dynamics, supply chain restructuring opportunities, and the stable demand in high-end segments to cope with the structural opportunities and challenges in the overall weak balance environment.

![[SMM Analysis] Futures Lack Momentum to Rise Further, Pre-Holiday Demand Stalls, and Stainless Steel Social Inventory Accumulation Intensifies](https://imgqn.smm.cn/usercenter/HBsPu20251217171723.jpeg)